At Miller & Newberg, we are committed to providing our clients with the best possible information to make decisions that help their businesses prosper. COVID-19 is a classic example of a risk that impacts the entire industry, and company executives naturally wonder whether what is happening at their company is happening to the same extent with their peers, and what should they do about it?

As the fourth largest annuity and life insurance actuarial firm in the U.S. and Canada based on the magnitude of our client companies’ reserves, and the third largest firm based on the number of client companies, our data at Miller & Newberg is very credible when it comes to insured lives mortality.

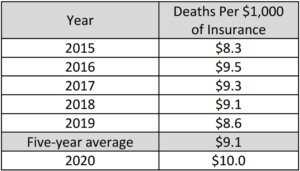

Most of our client insurance companies and fraternal benefit societies are seeing their overall death claims remain elevated. In 2020, our client companies collectively experienced death claims 12% higher than a normal year, and 2021 was unfortunately slightly worse at 13% higher than normal:

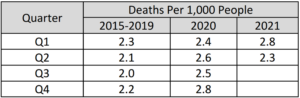

As to population mortality, looking at data from the CDC (the Centers for Disease Control and Prevention), in 2020, the United States experienced a death rate about 19% higher than a normal year, and 2021 was 21% worse than a normal year:

Whether companies realize it or not, their elevated death claims are almost certainly due to COVID-19, even if their internal data shows few claims listing COVID-19 on the death certificate.

The next question is, how should companies react? After all, if COVID-19 continued to cause elevated death rates throughout 2021 even though vaccines and better treatments were available, we should start to wonder whether product pricing needs to reflect this experience continuing.

We can see from the CDC data that COVID-19 deaths in the second half of 2021 were alarmingly close to the figures from one year prior.

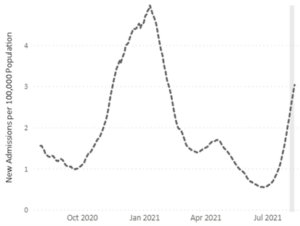

But as to what 2022 will bring, we see two very interesting facts when we look at CDC data on COVID-related hospital admissions. First, January 2022 was actually the single worst month for these hospital admissions since the pandemic started. But second, as of March 17, these hospital admissions were down 90% since their peak. See this chart, which was taken from \” https://covid.cdc.gov/covid-data-tracker/#new-hospital-admissions:\”

We conclude that COVID-19 death claims remain an issue for the life insurance industry, and we will likely see elevated death claims when first quarter 2022 results come in. But it is entirely possible that death rates hereafter will fall much closer to historical norms.

At this point, we have not seen the industry as a whole make any significant life insurance pricing changes as a result of COVID-19. Carriers are generally treating COVID-19 as a point in time event that will not change mortality over the long run. Time will tell, and Miller & Newberg will remain vigilant in tracking the data and helping our clients make the best decisions in light of it.